Understanding the Modern Monetary System

The modern monetary system has evolved into a complex structure that fundamentally shapes our economic and social realities. At the heart of this system lie critical questions: How is money created? Who benefits? and What impact does it have on the broader economy?

1.How Money is Created Today

In the modern economy, digital money is far more common than physical cash. Here are the key points:

Digital Money Dominates: 97% of the UK's money supply is made up of commercial bank money, meaning it exists digitally, in the form of electronic deposits. These digital figures are created by private banks when they issue loans. The remaining 3% is made up of physical currency like coins and notes, which we traditionally associate with money.

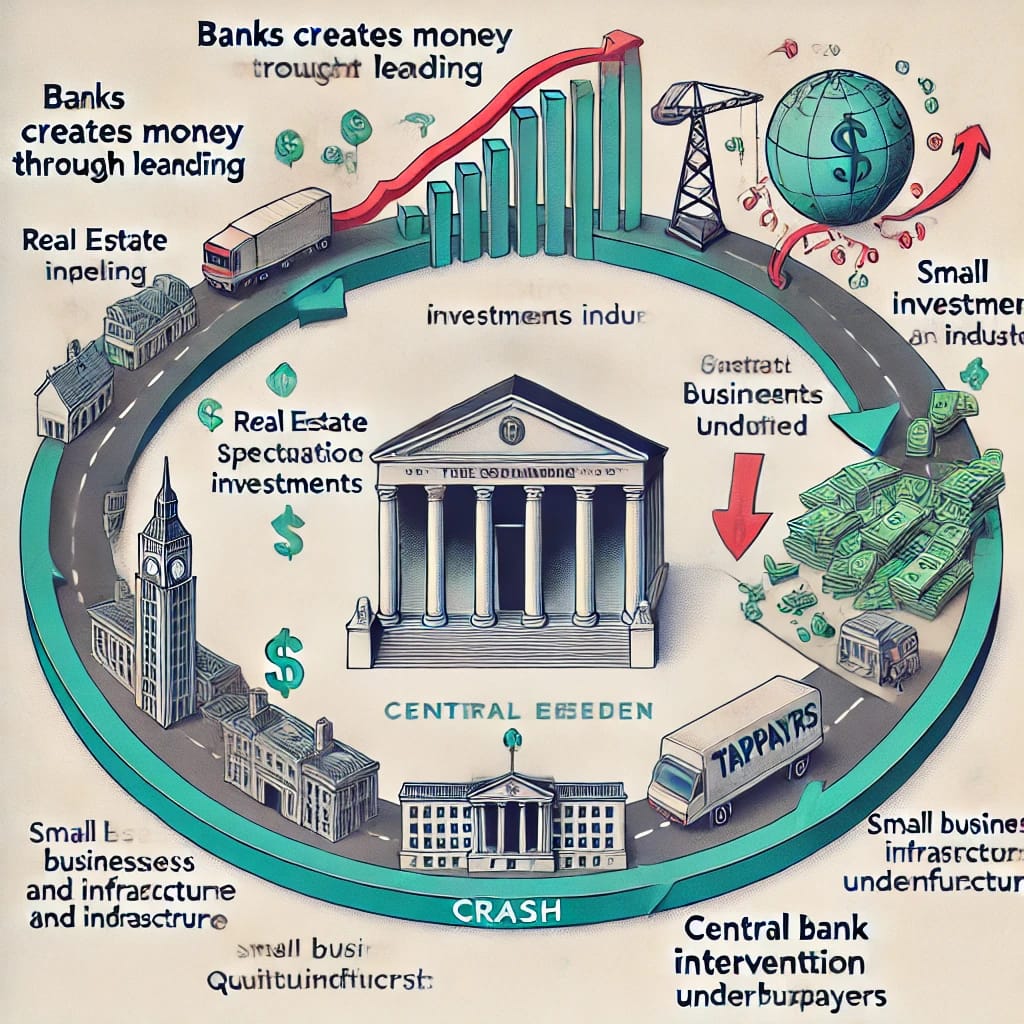

How Banks Create Money: Contrary to popular belief, banks don’t loan out money that people deposit into savings accounts. Instead, they create new money when they issue loans. Here’s how it works: When you borrow money from a bank, the bank doesn’t transfer someone else’s money to you. Instead, the bank makes an accounting entry in its system, increasing your account balance by the amount you borrow. This creates new money in the economy.

The Cycle of Money Creation and Destruction: Once a loan is issued and the borrower receives the money (in the form of a deposit), the new money enters circulation. However, as the borrower repays the loan, this created money is destroyed—it disappears from the system because loan repayments reduce the overall amount of money in the economy. Despite this, banks still profit from the interest that borrowers pay on top of the loan amount, which is where banks make most of their income.

Seigniorage: The Government’s Profit from Issuing Currency

Seigniorage refers to the profit that a government makes when it issues currency, particularly coins and notes. Here's how it works:

When the Bank of England prints a £10 note, the actual cost of printing might only be a few pennies.

However, the Bank of England sells this note to a commercial bank at its face value of £10, creating a significant profit margin. This difference—the face value of the note minus the production cost—is the government’s profit, known as seigniorage. This profit is transferred to the UK Treasury, which helps to reduce the amount of money that needs to be raised from taxes. Over the past decade, the UK Treasury has earned about £18 billion from seigniorage alone. This helps fund government expenses and reduces reliance on additional taxation.

By generating profit from printing money and selling it to banks, the government essentially creates a form of revenue without increasing the tax burden on the public.

2. Commercial Bank Money and the Digital Economy

Prior to the 19th century, there were various forms of money in circulation, such as coins made of precious metals, notes issued by local banks, and even barter systems. However, the modern monetary system has shifted almost entirely to digital money, most of which is created by commercial banks.

How Commercial Banks Create Money

Unlike central banks that control the issuance of physical currency, commercial banks create most of the money in circulation today. Here’s how:

Loans as Money Creation: When a commercial bank issues a loan, it doesn’t provide physical cash but instead credits the borrower’s account with newly created digital money. This money doesn’t previously exist in the economy; it’s created at the moment the loan is issued. For example, when you take out a mortgage to buy a house, the bank creates new money in the form of a digital deposit in your account. This is commercial bank money—money that exists digitally and is created as debt.

Digitalization’s Impact on Money Creation: With the increasing digitalization of the economy, the use of physical cash has diminished, and almost all transactions today occur digitally. This shift has concentrated the power of money creation in the hands of private banks, which can issue loans as they see fit. The amount of new money in the economy is no longer tightly controlled by central authorities (like the central bank) but rather by the lending activities of private commercial banks.

Consequences for the Economy

The concentration of money creation in the hands of commercial banks has several important consequences:

Economic Cycles of Boom and Bust: Because commercial banks create money by issuing loans, their profit motive encourages continuous lending. When times are good, banks tend to lend freely, leading to periods of rapid economic expansion (booms). However, this lending spree often leads to excessive debt, inflating asset bubbles (like housing or stock market bubbles). When these bubbles burst, banks stop lending, and the economy contracts, resulting in a bust. This cycle of boom and bust is partly driven by the role of banks in money creation.

Inequality in Wealth Distribution: The system of commercial bank money creation tends to favor certain sectors of the economy, especially those involving speculative investments like real estate and financial markets. Commercial banks prefer to lend to people and businesses that already have wealth or assets, because they are seen as safer investments. As a result, those who own assets (like property) benefit from rising prices, while those without assets find it increasingly difficult to afford basic necessities, such as housing. This can lead to widening inequality, as the rich get richer through access to easy credit, while others struggle to keep up with rising costs.

Reduced Control by Central Banks: While central banks like the Bank of England can influence the overall money supply by setting interest rates and conducting quantitative easing, they don’t directly control how much money is created on a day-to-day basis. This power now largely resides with private banks, whose lending decisions determine the amount of money circulating in the economy.

3. Historical Context: The Evolution of Money

The transition from a gold-backed currency to fiat money represents one of the most significant shifts in the history of modern economics. This transition fundamentally altered the way currencies work, moving from money being tied to a tangible asset like gold, to a system where money’s value is based solely on government decree and public confidence.

What is Gold-Backed Currency? In a gold-backed currency system (or the gold standard), a country's money is directly tied to a specific amount of gold. This means that a government could only issue money if it had the equivalent amount of gold reserves to back it up.

For example, if the US government printed a $100 bill, that bill represented an entitlement to a certain amount of gold. Citizens or foreign governments could, in theory, exchange the paper currency for its equivalent in gold at any time.

The gold standard was in place for most of the 19th and early 20th centuries and was widely seen as a way to keep inflation in check, since governments couldn’t print more money than they had gold to back it.

The Collapse of the Gold Standard and the Bretton Woods System:

After World War II, the global monetary system underwent a significant change with the establishment of the Bretton Woods Agreement in 1944. This agreement created a system where the US dollar was pegged to gold at a fixed rate of $35 per ounce of gold. Other currencies were then pegged to the US dollar, which created stability in international trade.

However, by the late 1960s, this system began to face serious problems:

The US had been printing more dollars to fund government spending, especially the Vietnam War and social programs, without increasing its gold reserves proportionally.

Countries began to doubt whether the US could actually back all the dollars it had printed with gold, leading to increasing pressure on the system.

In 1971, President Richard Nixon took the historic step of ending the convertibility of the US dollar into gold, effectively abandoning the Bretton Woods system. This event, known as the Nixon Shock, marked the transition to what we now know as a fiat money system.

What is Fiat Money?

Fiat money is currency that has no intrinsic value and is not backed by a physical commodity like gold or silver. Instead, its value comes solely from the fact that the government declares it as legal tender, and people trust it will hold value.

The word "fiat" comes from the Latin word for "let it be done" or "by decree," meaning that the currency has value simply because the government says so.

The Role of Trust and Belief

Since the end of the gold standard, the value of money is no longer tied to any physical commodity but is based entirely on trust in the government and the stability of the economic system.

The term credit, for example, comes from the Latin word "credere," meaning to believe. This highlights that the modern financial system is largely based on faith in the issuer of the currency—in most cases, the central government or central bank.

In the current system, when people exchange goods and services for money, they trust that the money will be accepted by others in the future and that it will retain its value over time. This belief is crucial because, unlike gold, fiat money doesn’t have any intrinsic value.

The Implications of Fiat Money

1. Monetary Flexibility:

The switch to fiat money gave governments and central banks much more flexibility in managing the money supply.

They can now print money without being constrained by gold reserves, which allows them to respond to economic crises by increasing the money supply or stimulating economic growth through monetary policy.

2. Inflation Risk:

One of the major downsides of fiat money is the risk of inflation. Since fiat money is not tied to a finite resource, governments can print too much money, leading to devaluation and a decrease in purchasing power.

Hyperinflation—where prices rise rapidly and currency becomes nearly worthless—has occurred in countries where governments printed excessive amounts of fiat money without economic backing (e.g., Weimar Germany, Zimbabwe, and Venezuela).

3. Economic Growth and Global Trade:

The shift to fiat money has supported unprecedented global economic growth. By allowing more flexibility in the supply of money, countries can more easily invest in infrastructure, expand businesses, and fund public services.

However, it also means that global economies are more interconnected, and crises in one country can affect others more quickly, since all currencies now float against each other without a common standard like gold.

4. Central Bank Power:

The role of central banks has become much more prominent in managing the economy. Central banks now control the supply of money through tools like interest rates, quantitative easing, and open market operations. This gives them significant power over inflation and economic stability.

4. Debt-Based Economy and Its Impact

In the modern banking system, money essentially equals debt. This might seem counterintuitive because we typically think of money as an asset. However, in today's economy, most money is created through the issuance of loans, which means that for there to be money in circulation, someone must take on debt.

Money Creation Through Debt

Here’s how the process works more explicitly:

1. Loans Create New Money:

When a bank issues a loan to a borrower, it doesn’t lend out pre-existing deposits from other customers. Instead, it creates new money. The bank credits the borrower’s account with the loan amount, even though no physical cash is moved or withdrawn.

This newly created money becomes part of the money supply, allowing the borrower to spend it. However, it also creates an equivalent amount of debt, which the borrower is obligated to repay, typically with interest.

2. Debt Fuels Money Circulation:

In this system, every time a loan is issued, new money enters the economy. This means that for the economy to have money circulating for day-to-day transactions, someone somewhere has to take on debt.

If no one took out loans, there would be far less money in circulation. This is because the majority of money exists digitally in bank accounts as deposits, which are created when loans are issued.

The Need for Ever-Increasing Levels of Debt

A crucial implication of this system is that a healthy economy depends on ever-increasing levels of debt:

1.Growing Debt to Maintain Economic Growth:

As more loans are issued, more money is created, which stimulates spending and investment, helping the economy grow.

However, to keep the economy functioning and to meet the growing demands for money, more and more debt must be taken on. This is particularly true in economies driven by consumer spending, where much of the growth comes from borrowing—whether through personal loans, mortgages, or business loans.

2. The Debt Trap:

Since the economy relies on debt to function, there’s constant pressure for more borrowing. But this creates a debt trap where debt levels must continually rise to keep the system going.

If borrowing slows down or if people start repaying their loans without new loans being issued, the amount of money in circulation can shrink, causing the economy to slow down.

Problems During Economic Downturns

This dependence on ever-increasing debt becomes particularly problematic during economic downturns:

1.Debt Becomes Unsustainable:

When the economy is growing, people and businesses feel confident borrowing and banks are willing to lend. But during a recession, when incomes fall, and businesses struggle, the burden of debt can become unmanageable.

If debt levels become unsustainable, borrowers may start defaulting on their loans, which leads to financial instability and forces banks to tighten lending. When banks stop issuing new loans, the money supply effectively shrinks, leading to a further contraction of the economy.

2. Recession Spiral:

In times of economic stress, the reduction in lending and borrowing can spiral into a deeper recession. With less money circulating, people spend less, businesses invest less, and the economy shrinks, which in turn makes it harder for borrowers to repay their debts, potentially leading to bank failures or credit crises.

Who Benefits? Banks and Financial Institutions.

While the modern system of money creation through debt is essential for economic growth, it tends to disproportionately benefit banks and financial institutions:

1. Interest Payments:

Banks make money by charging interest on the loans they issue. This means that while banks create money when they issue loans, they profit from the interest paid by borrowers. In fact, much of the wealth in the financial system is built on the interest income that banks and financial institutions earn.

Over time, as borrowers repay their loans with interest, the banks accumulate wealth, but the general public, particularly those who don’t have access to large loans or assets, may struggle to keep up with debt payments.

2. Concentration of Wealth:

The system tends to favor those who are already wealthy or have access to credit. Wealthy individuals and businesses can borrow large sums at favorable interest rates and invest in profitable ventures, further increasing their wealth.

In contrast, those without substantial assets often pay higher interest rates on smaller loans and may struggle to repay their debts, trapping them in a cycle of indebtedness. This leads to a growing wealth gap between those who can access and profit from the financial system and those who cannot.

Economic Inequality and the Banking System

One of the biggest criticisms of the modern banking system is that it exacerbates economic inequality:

Wealth Redistribution to the Financial Sector: As loans are repaid, the money created through borrowing is destroyed, but the interest paid on those loans remains with the banks. Over time, a significant portion of wealth in the economy is redirected to the financial sector, making banks and financial institutions richer while others face growing debt burdens.

Asset Price Inflation: When banks issue loans for real estate or financial assets, it drives up the prices of these assets. This benefits those who already own property or investments, as they see their wealth grow. However, for those who are trying to buy a house or invest in the market for the first time, rising prices make it harder to enter the market, further entrenching inequality.

5. Boom-Bust Cycles

The modern banking system's ability to create money through lending is a major driver of economic cycles of expansion and contraction, also known as boom and bust cycles. These cycles occur because the ease of borrowing money encourages speculative behavior during economic booms, but leads to crises and recessions when borrowers can no longer meet their debt obligations.

How Banks Create Money Through Lending

As discussed, banks create new money when they issue loans. When a borrower takes out a loan, the bank credits their account with the loan amount, effectively creating new digital money. This increases the money supply in the economy, fueling economic activity.

However, the downside is that the system encourages excessive lending, especially when economic conditions are good. During periods of growth, banks are more willing to lend, and borrowers are more willing to take on debt, particularly for purchasing assets like houses or stocks.

Boom Phases: Easy Access to Credit and Asset Bubbles

During the boom phase of the economic cycle, credit is easily available, and banks compete to issue more loans. The main drivers of this phase include:

1.Loose Lending Standards:

Banks, in their eagerness to profit from issuing more loans, may relax lending standards. They issue loans to borrowers who might not otherwise qualify, offering low-interest rates and minimal down payments.

This flood of easy credit encourages speculation—individuals and businesses borrow money not just to fund consumption or investment in productive activities but also to invest in assets like real estate or the stock market, hoping to profit from rising prices.

2. Asset Bubbles:

As more people borrow to invest in assets, demand for those assets increases, driving prices up. This creates what is known as an asset bubble.

For example, in the housing market, when banks offer easy mortgages, more people can buy homes. This increased demand pushes house prices higher, leading to house price inflation. People then begin to speculate on housing, buying homes as investments, expecting prices to keep rising.

The same phenomenon occurs in other markets like stocks, where cheap credit allows investors to buy more shares, driving stock prices higher and inflating the bubble further.

3.Excessive Debt Levels:

As asset prices rise, borrowers are encouraged to take on even more debt. For instance, as house prices rise, individuals may take out bigger mortgages or refinance their homes to access additional credit.

Businesses may also borrow more to expand operations or invest in speculative ventures, further inflating the bubble.

The Turning Point: Borrowers Can't Repay, and the Bubble Bursts

The problem with these boom cycles is that they are unsustainable. Eventually, the levels of debt become too high for borrowers to manage, and the bubble begins to burst:

1.Debt Repayment Becomes Unmanageable:

Many borrowers who took on loans during the boom, particularly at low-interest rates, start struggling to make repayments, especially if interest rates rise or if incomes fall during an economic slowdown.

Borrowers who speculated on asset prices rising (e.g., those who bought homes hoping to sell them at a higher price) find themselves overleveraged, meaning they owe more than the asset is worth if the bubble bursts and prices fall.

2.Defaults and Foreclosures:

When borrowers are unable to repay their loans, they default on their debts. In the housing market, this can lead to a wave of foreclosures, as banks seize properties to recover their losses.

As more homes or assets flood the market during a crash, prices plummet, causing the bubble to burst. The falling prices mean that borrowers who are still making payments may owe more on their loans than the asset is worth, a situation known as negative equity.

3. Widespread Economic Collapse:

The bursting of asset bubbles, particularly in sectors like housing, has ripple effects across the economy. Falling asset prices reduce consumer wealth, leading to a drop in spending and investment.

Banks, now burdened with bad debts and worthless assets (like homes that have lost value), become reluctant to issue new loans, leading to a credit crunch where borrowing dries up. This severely slows down economic activity, pushing the economy into a recession.

Government Intervention and Bank Bailouts

When these economic crashes happen, the fallout can be so severe that it threatens the entire financial system. As banks struggle with huge losses from bad loans and falling asset prices, they can become insolvent—unable to meet their obligations. This is where government intervention becomes necessary:

1.Bailing Out Banks:

In order to prevent a total collapse of the financial system, governments often step in to bail out banks. This involves providing emergency funds, often in the form of taxpayer money, to keep banks from going under.

For instance, during the 2008 global financial crisis, governments around the world, including the United States and the United Kingdom, used billions of dollars of public funds to bail out failing banks.

These funds are intended to stabilize the banking system, prevent further bank failures, and ensure that depositors don’t lose their savings.

2.Transferring Risk to Taxpayers:

While these bailouts help stabilize the economy, they also come at a significant cost to the public. The risk and financial burden of saving the banks are effectively transferred to taxpayers.

Instead of banks bearing the full responsibility for their risky lending practices, public funds are used to absorb their losses. This creates a situation where the general public pays the price for the mistakes made by the financial sector.

3.Moral Hazard:

The practice of bailing out banks also creates what is known as moral hazard. This refers to the idea that if banks know they will be bailed out in a crisis, they are more likely to take excessive risks during boom periods.

Knowing that the government will intervene if things go wrong, banks might feel less pressure to be cautious in their lending practices, which sets the stage for future economic bubbles and crises.

6. Quantitative Easing and Central Bank Policy

Quantitative Easing (QE) is a monetary policy tool that central banks, like the Bank of England, use during financial crises or periods of slow economic growth. It is particularly employed when traditional methods of stimulating the economy, such as lowering interest rates, have already been exhausted or are ineffective. Here's a more detailed and explicit breakdown of how Quantitative Easing works and its broader implications:

How Quantitative Easing (QE) Works

1. Creation of Central Bank Reserves:

To initiate QE, the central bank, such as the Bank of England, creates new central bank reserves. These are essentially electronic funds that the central bank adds to its balance sheet.

Unlike regular money, which is used by households and businesses for transactions, central bank reserves are only used between banks and the central bank itself.

2.Purchasing Financial Assets:

With these newly created reserves, the central bank begins to purchase financial assets from commercial banks and other financial institutions. The most common assets purchased in QE are government bonds (such as UK gilts) and, in some cases, corporate bonds.

The process goes as follows: the central bank buys bonds or other financial assets from commercial banks, and in return, those banks’ accounts at the central bank are credited with the new reserves. Essentially, the central bank is swapping bonds (which are less liquid) for more liquid reserves (money that can easily be lent out).

3. Increasing the Money Supply:

Through these purchases, the central bank injects liquidity into the banking system. This effectively increases the money supply because banks now have more reserves. The goal is to encourage banks to lend more to businesses and consumers, which can stimulate investment, spending, and overall economic activity.

Additionally, by buying large amounts of bonds, the central bank increases the demand for those bonds, which raises their price and lowers their yield (interest rates). This is because bond prices and interest rates move inversely. Lower interest rates on bonds make borrowing cheaper for the government, businesses, and households, further encouraging lending and spending.

Goals of QE: Stimulating Economic Activity

Quantitative Easing is designed to address several specific problems in a struggling economy:

1. Encouraging Bank Lending:

When banks sell assets like bonds to the central bank and receive reserves in return, the hope is that they will use these reserves to make new loans. More lending to consumers and businesses can help stimulate demand for goods and services, boost investment in the economy, and support economic recovery during a recession or period of stagnation.

2.Lowering Interest Rates:

QE also works by pushing down long-term interest rates. When the central bank buys government or corporate bonds, their yields (or interest rates) fall. Lower yields make it cheaper for businesses and households to borrow money for investments, such as expanding businesses or buying homes.

By lowering borrowing costs, QE aims to boost consumption and investment, two key drivers of economic growth.

3.Raising Asset Prices:

By increasing the demand for financial assets like bonds, QE drives up their prices. This, in turn, can lead to higher prices for other assets, such as stocks, real estate, and commodities. Rising asset prices can create a "wealth effect" where individuals and companies feel richer and thus more confident to spend and invest.

4.Preventing Deflation:

Deflation, or a persistent fall in prices, can be disastrous for an economy because it encourages consumers to delay spending in anticipation of further price drops, leading to reduced economic activity. By increasing the money supply and raising demand, QE can help prevent deflation and support moderate inflation, which is typically seen as a sign of healthy economic growth.

Challenges and Risks of Quantitative Easing

While QE can be a powerful tool for stabilizing an economy in crisis, it comes with several significant risks and challenges:

1. Inflation:

One of the primary concerns about QE is that it can lead to inflation. When a central bank increases the money supply by creating new reserves, there is always the risk that too much money will chase too few goods and services, leading to rising prices.

If the central bank injects too much liquidity into the economy, it may lose control over inflation, potentially leading to hyperinflation in extreme cases.

2. Rising Asset Prices and Inequality:

QE tends to inflate asset prices, including those of stocks, bonds, and real estate. While this can create a wealth effect, it disproportionately benefits people who already own those assets, such as wealthy investors and property owners.

As a result, QE can exacerbate inequality, as the wealthy see their portfolios grow, while those who don’t own significant assets (e.g., renters or low-income individuals) don’t benefit to the same extent.

3. Diminishing Returns:

Another problem with QE is the possibility of diminishing returns. If a central bank implements multiple rounds of QE (as seen in the aftermath of the 2008 financial crisis), the effectiveness of each subsequent round might decrease.

In some cases, despite the central bank injecting huge amounts of liquidity into the financial system, banks may still not lend because they are worried about future risks or borrowers’ ability to repay loans. This phenomenon is sometimes referred to as "pushing on a string", where the central bank can flood the market with money, but it doesn’t necessarily lead to the desired increase in lending and spending.

4. Depreciation of the Currency:

By increasing the money supply, QE can sometimes lead to the depreciation of the country’s currency on international markets. A weaker currency can boost exports (since they become cheaper for foreign buyers), but it also makes imports more expensive, which can lead to imported inflation.

In addition, a falling currency can erode investor confidence in the economy, leading to capital outflows and further instability.

5. Financial Instability:

Some economists argue that by keeping interest rates low and encouraging investors to search for yield in riskier assets, QE may contribute to financial bubbles. For example, low interest rates can lead to speculation in the stock market or the housing market, potentially inflating new bubbles that could burst and cause future financial crises.

Examples of QE in Action

The Bank of England began using QE in response to the 2008 global financial crisis. Between 2009 and 2012, it injected £375 billion into the economy through the purchase of government bonds and other assets.

The Federal Reserve in the United States used QE extensively after the financial crisis, purchasing trillions of dollars in government bonds and mortgage-backed securities. The aim was to stabilize financial markets, lower long-term interest rates, and encourage investment and consumption.

7. Consequences of Money Creation

As banks create money largely through lending, they often prioritize speculative investments (such as property) over productive investments (like small businesses). This has led to significant imbalances in the economy, with wealth concentrated in certain sectors (e.g., housing markets) and other areas, such as industry and public infrastructure, underfunded.

The document discusses the real impact of credit expansion: between 1998 and 2007, the UK money supply tripled, with £1.2 trillion created by banks through lending. This boom in credit contributed to the financial crisis of 2008, as speculative bubbles formed and then burst.

8. Economic Inequality and Financial Imperialism

In modern economies, commercial banks play a dominant role in the creation of money, largely through the process of lending. However, the way banks choose to allocate these loans often has profound effects on the structure and stability of the economy. While banks have the power to direct credit toward different sectors, they tend to prioritize speculative investments, such as real estate and financial assets, over more productive investments that support innovation, small businesses, or public infrastructure. This skewed allocation of resources creates significant economic imbalances, which can exacerbate wealth inequality and destabilize key sectors.

How Banks Create Money Through Lending

As mentioned earlier, modern money is primarily created when banks issue loans. In doing so, they don't lend out pre-existing funds but create new money in the form of commercial bank deposits. This process gives banks substantial influence over where newly created money flows in the economy. Ideally, banks could use this power to fund productive investments—such as small businesses, new technologies, and public infrastructure—that create jobs, increase productivity, and contribute to long-term economic growth. However, the reality is often quite different.

Prioritization of Speculative Investments

Banks, being profit-driven institutions, are primarily motivated by risk and return. They tend to favor lending in sectors where the potential for short-term returns is high and where the perceived risk is lower. Property markets, especially residential and commercial real estate, are seen as safe and highly profitable investments for several reasons:

Asset security: Loans secured against physical assets like property are less risky for banks because, in the case of default, the bank can seize and sell the property to recover its money.

High demand: In many developed economies, demand for housing continues to rise, pushing up prices and making real estate a highly attractive and liquid asset.

Market dynamics: Real estate markets often experience price inflation, meaning that the value of property tends to increase over time, creating further incentives for banks to lend more to property buyers.

As a result, banks direct large amounts of credit toward real estate and other speculative investments (such as stocks and financial derivatives) because these sectors offer a quicker and safer return on investment.

Consequences of Prioritizing Speculative Investments

1. Asset Bubbles and Market Instability:

When banks concentrate their lending on speculative sectors like housing, it can lead to the formation of asset bubbles. As more people take out loans to buy property, demand increases, pushing prices higher and higher. Eventually, these inflated prices become unsustainable.

When the bubble bursts—often triggered by rising interest rates or a sudden decrease in demand—property values crash, leading to widespread defaults on loans, a reduction in consumer wealth, and a contraction of economic activity. This is what happened in the 2008 financial crisis, where a housing bubble in the United States, fueled by easy credit, led to a global economic downturn when it collapsed.

2. Wealth Concentration:

The prioritization of speculative investments like real estate tends to concentrate wealth in certain sectors, particularly among wealthy property owners and investors. As housing prices rise, those who already own property benefit from rising asset values, while those who do not—often younger or lower-income individuals—are priced out of the market. This contributes to rising inequality, as the rich get richer through capital gains on assets, while others struggle to afford housing or access credit for more productive uses.

This phenomenon also leads to the financialization of the economy, where financial markets and asset ownership play a larger role in wealth generation than traditional industries like manufacturing or services.

3. Underfunding of Productive Sectors:

The over-concentration of lending in speculative sectors means that other parts of the economy—such as small businesses, manufacturing, public infrastructure, and innovation—are underfunded.

Small businesses, which are vital for job creation and economic dynamism, often find it harder to access credit because they are perceived as riskier compared to property investments. This can stifle entrepreneurship and innovation, preventing the economy from diversifying and growing in a sustainable manner.

Similarly, investment in public infrastructure—such as transportation, energy systems, and public services—often takes a backseat. This can result in long-term economic inefficiencies, as poor infrastructure hampers productivity, increases costs, and reduces the overall competitiveness of the economy.

4. Distorted Economic Growth:

By focusing on speculative investments like real estate, the economy becomes disproportionately dependent on asset price inflation rather than productive growth. This means that GDP growth might look strong, but it’s not necessarily being driven by increased production or innovation. Instead, much of the growth comes from rising property prices and financial speculation, which do not create new wealth but merely redistribute existing wealth.

5. Public and Social Costs:

When banks concentrate lending on housing markets, the cost of housing rises, making homeownership less affordable for the average person. This leads to housing crises, where many people are priced out of the market, forced to rent at high prices, or rely on social housing.

In turn, this creates a demand for government intervention to provide affordable housing or manage social inequality, adding further burdens on public finances. Meanwhile, speculative investors and banks that helped inflate housing bubbles can walk away with profits, leaving ordinary citizens and governments to deal with the consequences.

Potential Solutions: Redirecting Investment to Productive Uses

To address these imbalances, policymakers and central banks can take steps to redirect credit away from speculative sectors and toward productive investments:

1. Regulating Bank Lending:

Governments could regulate bank lending practices to encourage more loans to small businesses, innovation sectors, and infrastructure projects. For example, they might require banks to allocate a certain percentage of their lending portfolios to productive sectors or introduce incentives such as tax breaks or loan guarantees for banks that lend to small businesses and startups.

2. Investment in Public Infrastructure:

Governments can also step in directly to invest in public infrastructure. By increasing spending on transport systems, renewable energy, education, and health services, they can stimulate long-term economic growth, create jobs, and reduce the economy’s dependence on speculative financial sectors.

3. Financial Reforms:

Financial reforms, such as higher capital requirements for real estate loans, can reduce the amount of money flowing into speculative sectors. Reforms that promote greater transparency and reduce speculative activity in financial markets would help ensure that credit is used in ways that benefit the broader economy rather than just inflating asset bubbles.

4. Supporting Small Businesses:

Policymakers can support small businesses by providing more access to credit, either through government-backed loan programs or by encouraging alternative financing mechanisms, such as crowdfunding and peer-to-peer lending, which can bypass traditional banks.

Conclusion: The Future of the Monetary System

The modern monetary system, as it stands today, is primarily based on debt creation. The majority of money circulating in the economy is not physical cash, but rather digital money created when banks issue loans. This system is heavily reliant on continuous borrowing, which inherently ties the availability of money to the accumulation of debt. While this process allows for economic expansion and growth during boom periods, it also creates significant risks and vulnerabilities, particularly during downturns, when high levels of debt can become unsustainable.

This has resulted in a cycle of economic instability marked by periods of rapid expansion followed by financial crises, recessions, and rising inequality. As banks create money by issuing loans, they prioritize profit-driven decisions that often overlook broader social and economic impacts. This makes reform not just desirable but necessary to address the inefficiencies and inequities that are embedded within the current system.

The Debt-Driven Nature of the Current System

At its core, the current monetary system hinges on the fact that money is created as debt. Every time a bank lends money, new money is introduced into the economy, but at the same time, the borrower is responsible for repaying the loan with interest. The more money that circulates in the economy, the more debt is created, which means that for an economy to keep growing, debt levels must continuously increase.

However, this system creates a fundamental paradox. On the one hand, money is essential for economic activity—people need it for consumption, businesses need it for investment, and governments need it for public services. On the other hand, since money creation is tied to debt, this system means that economic growth is also tied to increasing levels of indebtedness. When debt levels become too high, and individuals, businesses, or governments can no longer service their debts, the result is economic contraction, or even financial crises.

Economic Instability and Boom-Bust Cycles

The debt-fueled nature of the system leads to boom-bust cycles, where easy access to credit fuels economic expansions, often leading to over-leveraging and the creation of asset bubbles. When the economy is doing well, banks are more willing to lend, and borrowers are more willing to take on debt. This cycle increases demand for goods and services, pushing up prices, inflating assets like property, and creating a false sense of security about future growth.

However, when these debt levels become unsustainable, whether due to rising interest rates, declining asset values, or external shocks, the system quickly unravels. Borrowers default on loans, the value of collateral (like homes or businesses) plummets, and banks reduce lending. The resulting credit crunch shrinks the economy, triggering recessions or financial crises, as seen during the 2008 global financial crisis. This cycle of expansion and contraction perpetuates economic instability, undermining long-term sustainable growth.

The Need for Reform

The current system, driven by debt and profit motives, benefits financial institutions and the wealthy far more than the general public. Banks, which are responsible for the creation of most money, tend to direct their lending toward speculative activities, such as real estate or financial markets, where the potential for short-term profits is high. This has the effect of inflating asset bubbles, concentrating wealth in the hands of a few, and exacerbating inequality. Meanwhile, productive investments in sectors such as small businesses, manufacturing, or public infrastructure are often neglected.

To address these inefficiencies and economic inequalities, reforming the monetary system is crucial. Below are several potential solutions:

1. Better Regulation of Bank Lending

A key reform would involve implementing stricter regulation on how banks allocate their lending. Currently, banks often prioritize lending to sectors that are seen as safer and more profitable, such as real estate, rather than sectors that generate long-term economic growth and societal benefits. By incentivizing banks to allocate a greater share of loans to productive investments, such as small businesses, green technologies, or public infrastructure, the broader economy could benefit from more balanced growth.

Governments could also introduce measures that prevent excessive speculation and reduce the formation of asset bubbles. For example, increasing capital requirements for speculative lending or taxing speculative investments could discourage banks from concentrating their resources in high-risk areas like real estate markets.

2. Separation of Money Creation from Profit-Driven Banks

Another approach to reform is the idea of separating money creation from profit-driven banks. Currently, the ability to create money is concentrated in the hands of private banks, which prioritize their own profitability. This system means that banks, rather than public institutions, have control over the supply of money in the economy, and their lending decisions are driven by short-term gains rather than the long-term health of the economy or society.

One proposed solution is the introduction of a public money creation system, where an independent public institution, such as a central bank, is responsible for creating money. Under this model, commercial banks would still exist, but they would only be able to lend pre-existing money rather than creating new money themselves. By taking money creation away from private banks, the economy could become less prone to boom-bust cycles, and money could be allocated more equitably across different sectors.

3. Democratic Control Over Money Creation

A more democratic approach to money creation could also be a critical reform. Rather than leaving decisions about money supply and lending to private banks, which operate with little public oversight, money creation could be subject to democratic control. This would mean that elected officials or publicly accountable institutions would have more say in where and how money is allocated in the economy.

By involving citizens and policymakers in decisions about money creation, it would be possible to ensure that money serves the broader interests of society rather than just the financial sector. For example, money could be directed toward socially valuable investments, such as affordable housing, renewable energy, education, and healthcare, rather than inflating the value of financial assets.

4. Central Bank Digital Currencies (CBDCs)

Another potential solution that has gained traction in recent years is the introduction of central bank digital currencies (CBDCs). A CBDC is a digital form of central bank money that could be used by individuals and businesses as an alternative to commercial bank deposits. If widely adopted, CBDCs could reduce the reliance on commercial banks for money creation, allowing central banks to have greater control over the supply of money in the economy.

CBDCs could also promote financial inclusion by providing people with access to safe and secure money without the need to rely on commercial banks, which often charge fees or impose high barriers to entry. This could make the financial system more equitable and reduce the concentration of power in the hands of a few large financial institutions.

The current monetary system, with its reliance on debt and profit-driven money creation, has resulted in cycles of economic instability and growing inequality. Reform is necessary to ensure that money serves the broader economy and society, rather than just the financial sector. Whether through better regulation of bank lending, the separation of money creation from private banks, or the introduction of democratic control over money supply, significant changes are needed to build a more stable and equitable financial system. By addressing these systemic issues, policymakers can help create a more resilient economy that benefits all members of society, rather than just a privileged few.

Comments

Post a Comment